The commentariat’s announcement last week that the New Zealand economy was in an ‘official recession’ by March 2023 – two quarters of output/GDP decline – was greeted with white faces by officials in the Reserve Bank and Treasury. There was queuing for the lavatories; some of the forecasters handed in their resignations to the Minister of Finance; one or two tested the windows to see whether they could jump out.

OF COURSE NOT. The officials would have been puzzled by the term ‘official recession’, since neither institution nor Statistics New Zealand (SNZ) use it. Later the commentariat changed the term to ‘technical recession’; I doubt any serious economist has the foggiest idea what a ‘non-technical recession’ is.

Instead, like me, the officials would have turned to their forecasts. The Treasury quarterly track in their Budget Economic and Fiscal Update (BEFU) forecast had a March 2023 increase of 0.3 percent instead of the 0.1 percent fall, so the economy appears to be tracking lower than they expected.

However, there is measurement error. One source of the error is that numbers inevitably bump around in a small economy (not to mention the complications from Easter being a moveable feast); another is that in order to publish the data early enough some, of the data input are estimates which will be updated when better figures come in. Based on the evidence of recent revisions, the March quarter could turn out to be mildly positive.

Unquestionably the economy is neither booming nor troughing; the cautious judgement – unlikely to be headlined by the media – is that the economy is flat or stagnating. If performance is measured by per capita output, the fall is somewhat larger since population has increased by about 1 percent in the two quarters.

Perhaps more important about the SNZ release was the contracting industries. Because of quarterly measurement and volatility, I looked at the year-on-year change. Negative growth is largely confined to agriculture, forestry, and fishing, mining and manufacturing – the tradeable sectors. That is not really good news because, some services such as tourism (which is not doing very well either) aside , they are the main contributors to foreign exchange earning and saving (import substitution).

I imagine there was a vigorous discussion within the Reserve Bank and Treasury between those who thought the data indicated the economy was contracting faster than expected, those who thought it was contracting earlier than expected, and the wait-and see-faction (which I probably would have belonged to). Some of the discussion would have been about the extent to which the RBNZ’s measures were working – perhaps faster than expected.

There may well have been more discussion in informed quarters on the previous day’s SNZ release on the balance of payments. It reported that in the year ended 31 December 2022 the current account deficit of $34.4 billion (9.0 percent of GDP) compared to $24.2 billion in the year ended 31 March 2022. It is the biggest deficit for the 20 years that SNZ reported.

SNZ attributed the main components of the deficit to a $6.4 billion widening of the goods deficit and a $2.2 billion widening of the primary income deficit. The primary income deficit indicates that New Zealand investors earned less overseas than overseas investors earned from New Zealand.

The above has focused on sectoral flows. Combining them, last year we borrowed more than in any year for two decades. Our net international liabilities have been rising.

Back to the BEFU forecast. There are some complications in interpreting their figures, but my reading is that the current account deficit is bigger than Treasury was forecasting – more than one could explain by data problems.

That means that in various places in the economy, sectors and households are borrowing to sustain their expenditures. We do not have the comprehensive investment and savings account to identify exactly where. We know that some of the borrowing is in the public sector, but that is only a partial explanation. Some will be for productive investment, some for residential housing purchases, and probably there are households who are borrowing or running down their savings.

Part of the worry has to be that with the economy stagnant or depressed, one might expect the savings deficit to increase as the economy begins expanding again – perhaps in early 2024.

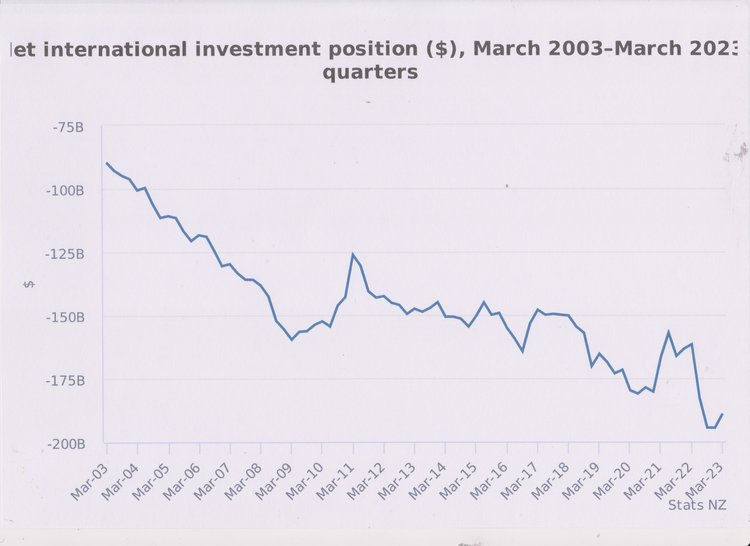

However, as I worked through the data I was struck by the SNZ graph which showed the net international investment position – how much we owe overseas (net). We owed $90b odd, in March 2003; as we borrowed more, the debt increased to $160b just before the Global Financial Crisis. After that shock the overseas debt stabilised and was $150b in March 2018. Since then, it has begun increasing again and is about $190b today. (There was some recovery in 2021. COVID?)

It is all very well saying that most of this debt is private and not a matter for public policy. We saw how in the GFC, the private debt of the commercial banks became a public concern. I have no doubt that at our next credit rating review, officials will be pressed by the credit rating agencies. The resulting rating guides the international investors who are lending to us. If the officials don’t have a satisfactory response, the interest rates at which we borrow internationally will be higher, including feeding through to those on residential mortgages.

One of the lessons from New Zealand’s economic history is that our big economic crises have usually been associated with our overseas debt. Of course, I may be wrong next time; the ostriches do not expect another major crisis here or globally. But it seems to me that the debt level issue is far more important than the commentariat wittering away about whether we are in a recession, be it ‘official’, ‘technical’ or just an old-fashioned downturn.

Click to view

Brian Easton is an economist and historian from New Zealand. He was the economics columnist for the New Zealand Listener magazine for 37 years. This article was first published HERE

However, there is measurement error. One source of the error is that numbers inevitably bump around in a small economy (not to mention the complications from Easter being a moveable feast); another is that in order to publish the data early enough some, of the data input are estimates which will be updated when better figures come in. Based on the evidence of recent revisions, the March quarter could turn out to be mildly positive.

Unquestionably the economy is neither booming nor troughing; the cautious judgement – unlikely to be headlined by the media – is that the economy is flat or stagnating. If performance is measured by per capita output, the fall is somewhat larger since population has increased by about 1 percent in the two quarters.

Perhaps more important about the SNZ release was the contracting industries. Because of quarterly measurement and volatility, I looked at the year-on-year change. Negative growth is largely confined to agriculture, forestry, and fishing, mining and manufacturing – the tradeable sectors. That is not really good news because, some services such as tourism (which is not doing very well either) aside , they are the main contributors to foreign exchange earning and saving (import substitution).

I imagine there was a vigorous discussion within the Reserve Bank and Treasury between those who thought the data indicated the economy was contracting faster than expected, those who thought it was contracting earlier than expected, and the wait-and see-faction (which I probably would have belonged to). Some of the discussion would have been about the extent to which the RBNZ’s measures were working – perhaps faster than expected.

There may well have been more discussion in informed quarters on the previous day’s SNZ release on the balance of payments. It reported that in the year ended 31 December 2022 the current account deficit of $34.4 billion (9.0 percent of GDP) compared to $24.2 billion in the year ended 31 March 2022. It is the biggest deficit for the 20 years that SNZ reported.

SNZ attributed the main components of the deficit to a $6.4 billion widening of the goods deficit and a $2.2 billion widening of the primary income deficit. The primary income deficit indicates that New Zealand investors earned less overseas than overseas investors earned from New Zealand.

The above has focused on sectoral flows. Combining them, last year we borrowed more than in any year for two decades. Our net international liabilities have been rising.

Back to the BEFU forecast. There are some complications in interpreting their figures, but my reading is that the current account deficit is bigger than Treasury was forecasting – more than one could explain by data problems.

That means that in various places in the economy, sectors and households are borrowing to sustain their expenditures. We do not have the comprehensive investment and savings account to identify exactly where. We know that some of the borrowing is in the public sector, but that is only a partial explanation. Some will be for productive investment, some for residential housing purchases, and probably there are households who are borrowing or running down their savings.

Part of the worry has to be that with the economy stagnant or depressed, one might expect the savings deficit to increase as the economy begins expanding again – perhaps in early 2024.

However, as I worked through the data I was struck by the SNZ graph which showed the net international investment position – how much we owe overseas (net). We owed $90b odd, in March 2003; as we borrowed more, the debt increased to $160b just before the Global Financial Crisis. After that shock the overseas debt stabilised and was $150b in March 2018. Since then, it has begun increasing again and is about $190b today. (There was some recovery in 2021. COVID?)

It is all very well saying that most of this debt is private and not a matter for public policy. We saw how in the GFC, the private debt of the commercial banks became a public concern. I have no doubt that at our next credit rating review, officials will be pressed by the credit rating agencies. The resulting rating guides the international investors who are lending to us. If the officials don’t have a satisfactory response, the interest rates at which we borrow internationally will be higher, including feeding through to those on residential mortgages.

One of the lessons from New Zealand’s economic history is that our big economic crises have usually been associated with our overseas debt. Of course, I may be wrong next time; the ostriches do not expect another major crisis here or globally. But it seems to me that the debt level issue is far more important than the commentariat wittering away about whether we are in a recession, be it ‘official’, ‘technical’ or just an old-fashioned downturn.

Click to view

Brian Easton is an economist and historian from New Zealand. He was the economics columnist for the New Zealand Listener magazine for 37 years. This article was first published HERE

2 comments:

Is a recession the worst of our worries? NO

Who in Hell Gives the UN, WHO and the EU the Right to Impose Digital Vaxx Certificates? The answer imposes itself: The devil himself. Because there is no international law allowing such human tyranny. This is an elite-made “rules-based order” striking down any dictatorial, military-enforced command on humanity.

That’s what the West has become since the Covid fraud, an empire led by evil itself.

The West has not just become a sea of criminal institutions, if not stopped NOW, it will continue with its drive to complete its eugenics and transhumanism agenda – way before 2030.

We, the People, must stand up NOW against this tyrannical attempt by foremost three key institutions to dominate, enslave and tyrannize to death most of the commons of world populations.

The UN, WHO, EC / EU – and of course, the WEF, diabolical institutions by nature and their leadership cannot be reformed, but must be dismantled for the sake of humanity.

Insight must be sufficiently powerful to open people’s eyes and ears, to mobilize them to action in SOLIDARITY, taking measures in spirit and unison, not in violence, but in deeds that vibrate worldwide at a level where a collapse into a civilization-ending abyss may be avoided.

“There is a crack in everything where the light shines through.”

Peter Koenig

And lets not forget the Council For Inclusive Capitalism,the top dog of them all.

Post a Comment

Thank you for joining the discussion. Breaking Views welcomes respectful contributions that enrich the debate. Please ensure your comments are not defamatory, derogatory or disruptive. We appreciate your cooperation.