But this one caught my eye.

Just before the last MPS a few weeks ago the Bank sent out a routine advisory about post-MPS engagements senior managers would be doing. It included this snippet

Click to view

Quite probably no one much outside Queenstown and lakes area gave it another thought. The clear implication was that there’d be nothing new or newsworthy in what the Governor was saying.

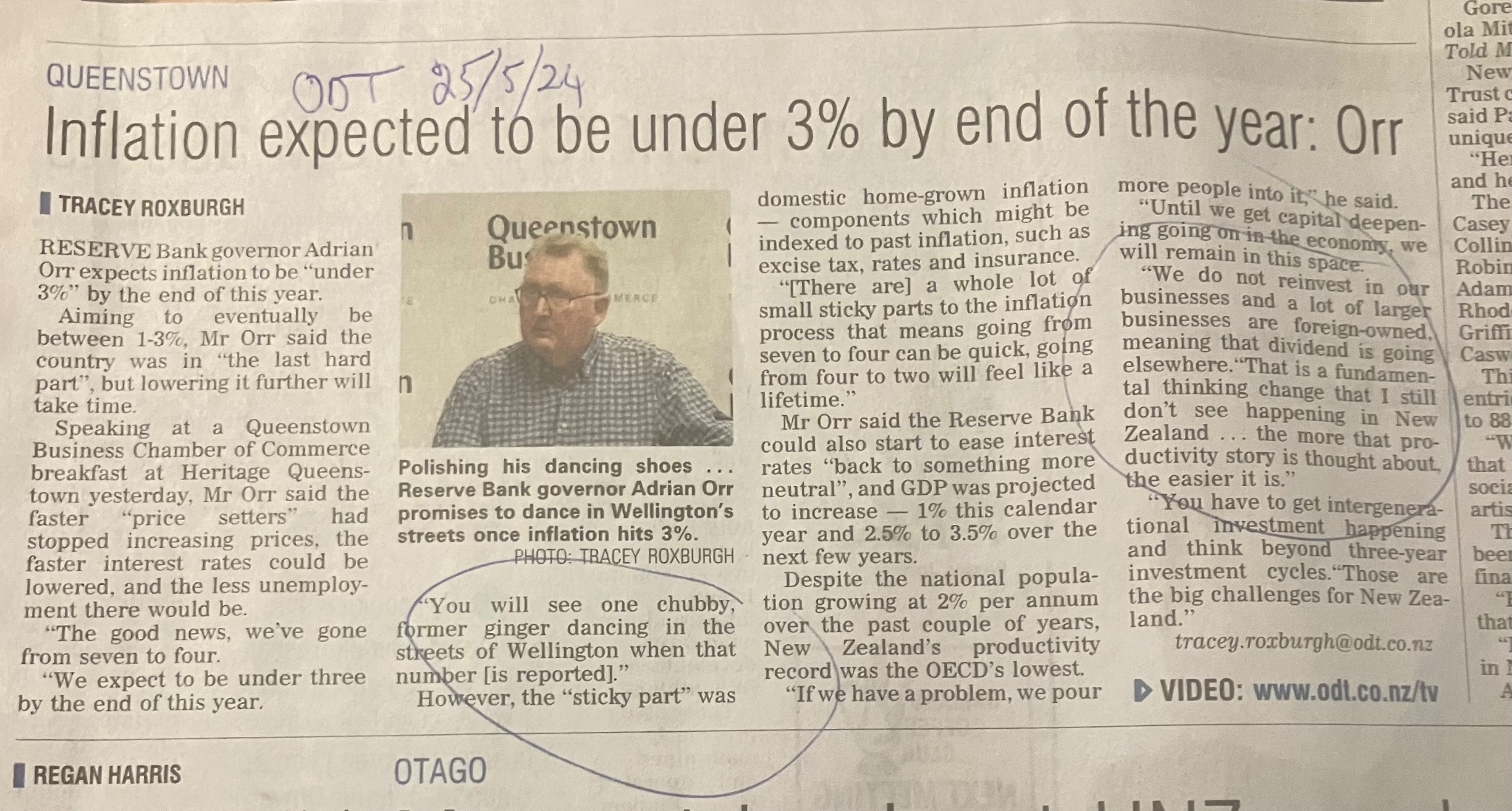

But I happened to be in Dunedin a couple of days later, where I stumbled on this article in the local paper

Click to view

which made it quite clear that even if Orr had been using presentation slides from the MPS that hadn’t come even close to being the limits of what he’d said.

Again, there were a few things that caught my eye.

First, there was that weird – but not new from Orr – suggestion that “price setters” might choose to alter their behaviour to help out the Bank. Rather odd really. Not only do those firms have shareholders to whom they owe legal duties, but next time inflation undershoots the target midpoint should we expect the Governor to be urging firms to make a bit more profit by helping him out and raising their prices? Charitably, I guess that probably wasn’t what he had in mind, but whatever his intent he feeds a narrative in which core inflation is anyone’s responsibility other than the Bank’s and MPC’s.

Then there was that crass line about “you’ll see one chubby former ginger dancing in the streets of Wellington when that number [inflation under 3 per cent] is reported”. I’m guessing those whose businesses were closed down, those whose jobs were lost in the process, probably won’t be sharing in the Governor’s jubilation.

Look, I’m quite sure the Governor will genuinely be pleased when inflation is below 3 per cent – hopefully, even more so when it gets near the 2 per cent midpoint he is required to focus on – but this is the same Governor who has never expressed even a shred of contrition for his part in the inflation (let alone those huge, utterly unnecessary losses – which would have paid for many many (eg) cancer drugs). It was the sort of juvenile line one might expect from a junior official. From a Governor one might have hoped for a little more gravitas. Yes, even from Orr.

But what really prompted me to write this post was those comments on productivity, immigration, and related issues. Remarkably – and they really are quite remarkable comments from a long-serving advanced country central bank Governor – they’ve had no other coverage anywhere, and seem to have sparked no follow-up comments to (for example) the Minister of Finance, the person who is responsible to Parliament and public for the Reserve Bank and the Governor.

He is reported as having said that “New Zealand’s productivity record was the OECD’s lowest” in the last couple of years. I’m not sure quite which data he is using. but our productivity growth (or lack of it) has been pretty bad. In fairness so has productivity growth in a bunch of other OECD countries (the US tends to stand out at the other end of the scale). And this is, it seems according to the Governor, due to our immigration policy. Big news if true, especially when it comes from…..the Governor of the Reserve Bank (even if it is a matter for which he and the Bank have had no responsibility whatever). He goes on – and here we get quote marks – “if we have a problem, we pour more people into it”. Look, I have been quite vocal over the last decade or more on the way I think immigration policy has been systematically harming New Zealand’s (and Australia’s for that matter) longer-term productivity performance) but a) I’m just a private commentator, while he’s the Governor, and b) I don’t think even I’d be quite that reductionist, especially in a formal setting (like a speech from the central bank Governor).

And then he is reported as going on: “Until we get capital deepening going on in the economy, we will remain in this space” [presumably meaning low productivity growth]. Which is all rather mechanistic and not very insightful at all. There aren’t just lumps of capital that some central planner decides to allocate more of, but firms in markets, making profit-maximising choices against the backdrop of the opportunities they perceive and the regulatory etc environment governments impose.

And, to save you scrolling up and down, here is the crowning set of quotes

Not entirely clear who “we” is here, but presumably he means businesses operating in New Zealand taken as a whole. And note that his comment is about reinvestment, not investment per se (as it happens, total investment as a share of GDP has been higher in New Zealand most of the last 15 years than the median of the IMF grouping of advanced countries), so quite what is he on about? We know that New Zealand has a corporate tax system (dividend imputation) that does not generally double-tax profits earned by companies with New Zealand shareholders, and so – like Australia – tends to have quite high dividend payout rates. But what is the Governor’s beef? Is he seriously arguing for a more distortionary tax system, to stop companies distributing profits as readily? You might have thought that if he was going to weigh in on such issues he might have highlighted that we (and Australia) now have one of the highest company tax rates in the world, and company tax rates really bit on foreign investment (since foreign investors can’t use imputation credits).

But no. In fact, what we get from these comments is that the Governor isn’t very happy about the foreign investment we do have. In fact, unlike almost every serious economic commentator (and in fact the government), he seems to think there is too much of it, falling back on that rank populism beloved of the Greens, the left wing of the Labour Party…..oh, and the marketing department of TSB Bank (my photo from a few years ago). Oh no, the dividends are going to…..well, the people that provided the capital.

As it happened, when I looked up the detailed balance of payments data, there had been $21.4 billion of reinvested earnings by foreign-owned companies operating here in the five years to March 2023. Quite probably some of it was more or less compelled by Orr’s own OTT additional requirements for bank capital (the staggeringly expensive insurance policy that was never subject to a proper cost-benefit analysis) – and the banks are the biggest foreign investors (collectively) in New Zealand. But you are left wondering quite what Orr is on about, and based on what. Just more of the unedifying Australian bank-bashing that he has become known for (recall how keen he seemed when those capital proposals were around for one of the Australian banks to divest and throw their business on the tender mercies of the NZX).

But just what, substantively, was the Governor on about? And how did he conclude that it was his place – charged with delivering price stability (oops) and maintaining financial system stability – to be suggesting, and it does seem to be the implication, that really we’d be better off with less foreign investment? This the same Governor who in the same speech seemed (see above) to be lamenting the relative lack of capital investment in New Zealand.

The account in the ODT ends with a couple of rather cryptic comments. The first (“that is a fundamental thinking change…”) seems to relate to his lament about foreign-owned firms paying investors dividends – which is presumably what they do when they don’t have great investment opportunities presenting themselves here. But, according to Orr, somehow the answer lies there: on this count “the more that productivity story is thought about the easier it is”. What, we should discourage foreign investors and somehow prevail on those who remain to invest here even when it isn’t financially attractive to do so? I can’t imagine that that is really what he means, but it is certainly what it sounds like.

And then an old favourite of Orr’s – with almost nothing whatever to do with his actual responsibilities – is all that talk about needing “intergenerational investment”. One supposes that perhaps he had in mind really long-lived infrastructure projects – things New Zealand entities, many of them government ones, seem woefully bad at executing in a cost-effective way – but actually depreciation (whether of the market value of new ideas, or of physical capital) means that most investments anywhere are much shorter-lived than “intergenerational”. And if the Governor thinks he can be confident about what ‘intergenerational” opportunities are out there that private firms might sensibly lay hold off, perhaps he might reflect on his own state of knowledge about the things he’s actually responsible for. That inflation, for example, wasn’t exactly something he set out to deliver.

It really is woeful stuff coming from the Governor of the Reserve Bank. If one of his junior managers had gone off reservation with such thoughts at a briefing far from home one might put it down to youthful enthusiasm and inexperience. But this is one of the most powerful government officials in the land, the long-serving Governor of our central bank. And, sure, it no doubt wasn’t a fully scripted speech, but…..he was apparently on-the-record (and even if he wasn’t central bank Governors are supposed to speak guardedly, perhaps especially about things that aren’t their responsibility)….and the onus is on him when he speaks to speak well and not just throw out glib populist lines.

But it seems that – once again – there is no price to pay. The ODT journalist who wrote the story even had her email address in the article, so it would have been very easy for specialist political or business journalists to have followed up on these loose comments (and who knows what else he might have said – ODT readers probably having a limited appetite for reports of the Governor), but apparently not. No one seems to have challenged the Minister of Finance, about whether it was really appropriate for the Governor – who hasn’t been doing his day job well – to be masquerading as some sort of Green Party economic nationalist stand-in (but then just a week ago the same Minister told the press the Orr was not her responsibility – even though the Act explicitly says otherwise).

What does the rest of the world (markets and RB watchers) make of it? I guess if they didn’t happen to read the ODT they’d not have known.

Once again, it really isn’t good enough. Another government agency head still in place after failing badly (my 20 reasons why Orr should never have been reappointed, not then including the inflation numbers). And a government that seems to barely care (in Orr’s case, there is still no sign of any attempt to clip his wings – eg foreshadowing deep budget cuts, letters of expectations, forcing the MPC to be more open, appointing a Board chair who make actually represent the public interest etc; really just nothing).

There was an old line of Alan Greenspan’s that “if you think I have been particularly clear you have probably misunderstood what I said”. Orr, by contrast, straying beyond his bailiwick seems quite troublingly clear. Is there any other advanced country central bank Governor who is on record in recent times lamenting (simultaneously) the lack of investment in his economy, and the presence of too much FDI?

Michael Reddell spent most of his career at the Reserve Bank of New Zealand, where he was heavily involved with monetary policy formulation, and in financial markets and financial regulatory policy, serving for a time as Head of Financial Markets. Michael blogs at Croaking Cassandra - where this article was sourced.

2 comments:

Maybe Governor Orr was pleased Tiwai Smelter had committed to intergenerational investment in NZ with their announcement of a further 20 years operation as a leading smelter "price setter".

Southland is overjoyed that Tiwai is to continue supplying employment , GDP and confidence .

At times Orr comes across as if he is disappointed with his place in life. Rather than the governor of the RB, he sees himself as the rightful leader of our country. His speeches are those of a politician, explaining his plan to rescue our backward country, if only we would bend the knee.

As this hasn't happened, he has done the next best thing, with the help of our previous minister of finance, and created his own fiefdom. An ever increasing budget, with ever more subservient staff that continues to grow.

The fact he hasn't been smacked down for over stepping his remit makes me wonder what skeletons he knows about. Leverage is the only explanation. Or, perhaps, just more incompetence by the new team.

Post a Comment

Thank you for joining the discussion. Breaking Views welcomes respectful contributions that enrich the debate. Please ensure your comments are not defamatory, derogatory or disruptive. We appreciate your cooperation.