Who said this?

The world is awash with savings yet New Zealand does not provide a gateway that makes it easy for that capital to enter the country.

Well, that was one Christopher Luxon on the campaign trail three months out from the election last year.

At the time, Labour was in office. This was how their Minister of Finance had articulated the Labour government’s general attitude to foreign investment, in an official directive letter required by statute and addressed to Land Information New Zealand which runs New Zealand’s overseas investment regulatory regime

At the time, Labour was in office. This was how their Minister of Finance had articulated the Labour government’s general attitude to foreign investment, in an official directive letter required by statute and addressed to Land Information New Zealand which runs New Zealand’s overseas investment regulatory regime

Click to view

He went on to outline some caveats, and no one could accuse the 2017 to 2023 governments of being unequivocally keen on all and any foreign investment (they were, after all, the government of the ban on foreigners buying houses here).

But what of the Governor of the Reserve Bank? Normally, one might expect Governors to keep any opinions on FDI to themselves (once upon a time the Reserve Bank administered the relevant legislation, but no longer) or at very most to articulate something close to government policy. It isn’t, after all, their area of responsibility (debt inflows might be a different matter).

But this was what he told his Queenstown audience a couple of weeks ago, in a speech delivered in his official capacity

Our central bank Governor seems to be saying that there is something wrong with having so much foreign investment in New Zealand, and that it is somehow related to what holds back productivity growth in New Zealand?

As I noted in Saturday’s post, it really isn’t clear what he is on about or what he is basing these quoted comments on.

It isn’t, after all, as if New Zealand has a particularly large stock of inward foreign investment.

Click to view

In fact, among OECD economies we are in the bottom third, expressed as a percentage of GDP (the chart doesn’t show Ireland, Luxembourg or Netherlands which are off the scale to the right on account of company tax regime distortions – although the “true” level of FDI in each country will be quite large).

And New Zealand is well known for having a not-exactly-welcoming regulatory approach to foreign investment

Click to view

People debate quite what the New Zealand number really means in substance, but our governments don’t go out of their way to make it easy.

What about the current government? Well, as it happens, the Associate Minister of Finance with responsibility for the Overseas Investment Act issued a new one of those directive letters to LINZ just a few days ago. In his press release he noted:

Click to view

And in the official directive letter he wrote

Click to view

That seems pretty clear (although a shame about that absurd foreign buyers ban that is still in place).

But it seems to be utterly at odds with the public views, expressed in his official capacity, of the Governor of the Reserve Bank. Not only do Orr’s comments seem out of step with most conventional economic analysis and advice (I guess there is always the Greens and Bill Sutch of dubious memory on the other side), but – on a area in which he has no policy responsibility – quite out of step with the government. He has always been free to resign and run for Parliament or establish a think-tank. But for now he is a senior and very powerful official delegated huge powers (which, as it happens, he hasn’t even exercised well).

The Governor often likes to cite the, mostly meaningless (because it simply explains what the point of having the Bank is, and nothing about powers or specific goals), purpose clause in the Reserve Bank Act

Click to view

Both governments he has served under have stated that they see foreign investment as having an important role in helping lift prosperity etc. But not, it seems, the Governor.

Look, if at a private dinner party with close friends or over a beer with his mates Orr wants to muse in some neo-Sutchian or Green Party way then who are we to object (although even then good central bank Governors should be very guarded about what they say to anyone), but this was in an official speech in his official capacity. And if he reckons the ODT’s journalist has quoted him badly out of context, the onus should be on him to clear things up (but he is only likely to do so if journalists start asking him hard questions, of which there is no sign so far).

As a reminder, the Associate Minister of Finance making those foreign investment comments wasn’t just the minister actually responsible, but also the leader of the ACT Party, a senior Cabinet minister and someone who will be Deputy Prime Minister a year from now. He is also the author of a letter to the then Minister of Finance – who was required by his own new law to consult other parties in Parliament – strongly opposing the reappointment of Orr as Governor (page 15 here). There is no sign Orr has changed for the better (Seymour objected under three headings: Poor Leadership, Poor Outcomes, and Poor Focus – and you’d have to think Orr’s weird and unsubstantiated FDI comments fall smack within that third category).

It was always a bit staggering that Grant Robertson, having passed a law himself requiring that the other parties in Parliament be consulted on the appointment of a Governor (one could argue this was an amendment with merit, consistent with the idea that even if people didn’t always agree with a person serving as Governor at least it should be someone who commanded pretty wide-ranging respect across the political spectrum) went ahead and reappointed Orr over the explicit written objections of the two largest opposition parties, knowing that the law made it very difficult (probably rightly so) for him later to be dismissed if the government changed.

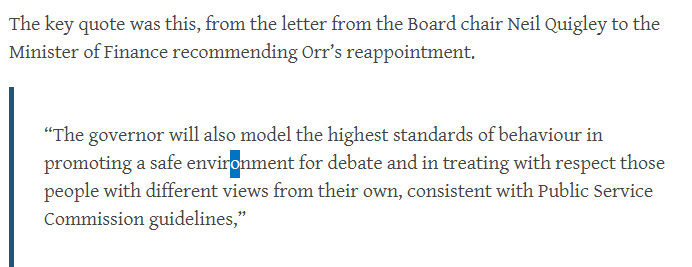

But Orr has shown no signs of buckling down and acting in a disciplined way that might command grudging respect from those who had been openly sceptical in his first term, even though that was the sort of line the egregious Reserve Bank Board chair used to make the case for reappointing his man

Click to view

We’ll see a new, different and better Orr next time round seemed to be the suggestion…..

Orr was back on form a couple of weeks ago with his abuse of banks and of the New Zealand Initiative, when the Initiative (a body to which the main banks belong) had the temerity to disagree with and criticise the Governor and his policies. He just doesn’t get the idea that reasonable people might differ from him, let alone that as a very powerful regulator he has particular responsibilities to operate in a restrained and disciplined manner, not by implication opening the possibility of taking out on regulated entities his vengeance for daring to openly disagree.

Fortunately perhaps, the ACT Party is not an entity regulated by the Governor. On their official Twitter account I spotted this 10 days ago

Click to view

Now, Todd Stephenson may be not much more than a backbencher BUT (a) he is actually a PPS to David Seymour, so not exactly marginal within ACT, and b) this statement (“he is temperamentally unfit as a steward of banking regulation”) is posted on the official Twitter account of a party that is a full member of the coalition government, a party headed by an Associate Minister of Finance no less. And, 10 days on, the post is still there (clearly wasn’t some junior staff’s fit of excess enthusiasm quickly pulled down by the powers that be).

It really is extraordinary that we have a central bank Governor:

- openly articulating views on foreign investment (something he has no responsibility for) apparently at odds with views of successive govts,

- attacking private entities for having the temerity to disagree with him, and implicitly holding over bank members of that body a reminder of all the regulatory power he wields over them,

- being openly attacked as unfit for office by a political party that is a component of the current coalition government, whose leader is an Associate Minister of Finance.

Click to view

(I don’t think it is plausible to use these powers to sack the Governor – I don’t think behaviour since March last year (his reappointment) rises safely to that level, and any attempt could be judicially reviewed, in a very messy and disruptive way, but……Orr is her problem, and she so far displays no sign of any interest.)

I might suggest it was all rather Third World, but that might be unfair to them. But it is rather unsatisfactory all round, and really needs sorting out (like so many aspects of our failing public sector). Journalists with access asking hard questions might be a good start.

Michael Reddell spent most of his career at the Reserve Bank of New Zealand, where he was heavily involved with monetary policy formulation, and in financial markets and financial regulatory policy, serving for a time as Head of Financial Markets. Michael blogs at Croaking Cassandra - where this article was sourced.

1 comment:

He wants to be dismissed, for kudos and payout

A woke fool running as an activist, does he believe Robertson was capable as a finance minister, well he did and finds it hard to admit he was stupid, so doubles down.

A disciplinary process should be started.

Post a Comment

Thank you for joining the discussion. Breaking Views welcomes respectful contributions that enrich the debate. Please ensure your comments are not defamatory, derogatory or disruptive. We appreciate your cooperation.